1 Introduction to AI in Finance

AI has moved from a peripheral idea in finance to a central force reshaping how institutions operate, compete, and make decisions. The text opens by showing that banks and other financial firms are not only adopting AI to automate tasks, but also to change the kinds of talent they need and the kinds of products and services they can offer. It emphasizes that finance is especially well suited to AI because it is fundamentally data-driven, with every loan approval, trade, fraud check, or customer interaction generating information that can be analyzed and acted on.

The chapter explains that financial AI is different from general AI because the stakes are higher: decisions affect money, risk, compliance, and fairness, so systems must be accurate, explainable, and adaptable. It organizes AI’s impact into four major areas: managing risk and compliance, extracting market intelligence, improving customer experiences, and increasing operational efficiency. Across these areas, AI helps institutions assess credit more dynamically, detect fraud more effectively, analyze large volumes of research and alternative data, personalize services, and automate repetitive work that once consumed significant human effort.

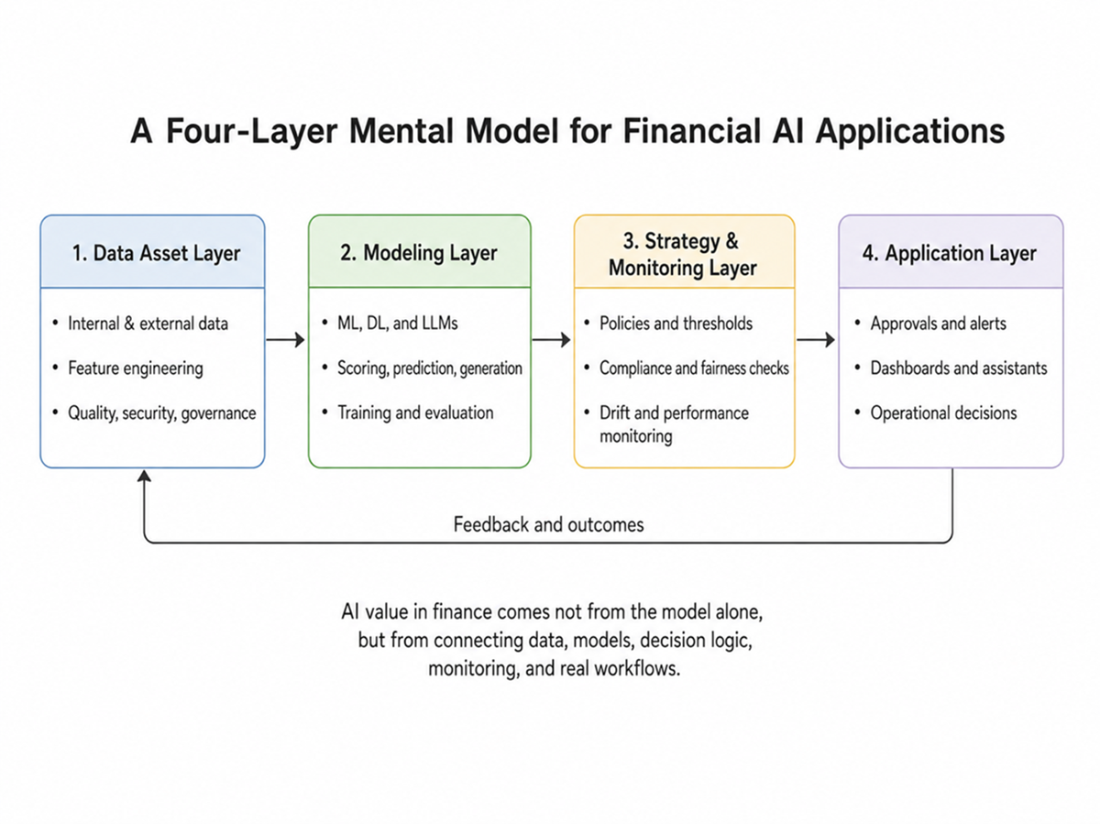

To make these ideas practical, the text introduces a four-layer model for building financial AI applications: data assets, modeling, strategy and monitoring, and application delivery. It then applies that framework to credit scoring, showing how raw internal and external data becomes a predictive model, how model outputs are governed by business and regulatory rules, and how those decisions are delivered in real workflows with feedback loops for ongoing improvement. The chapter closes by outlining the basic tools and infrastructure needed to work through the book’s examples, highlighting that common open-source technologies, standard laptops, and accessible datasets are enough to start building real financial AI systems.

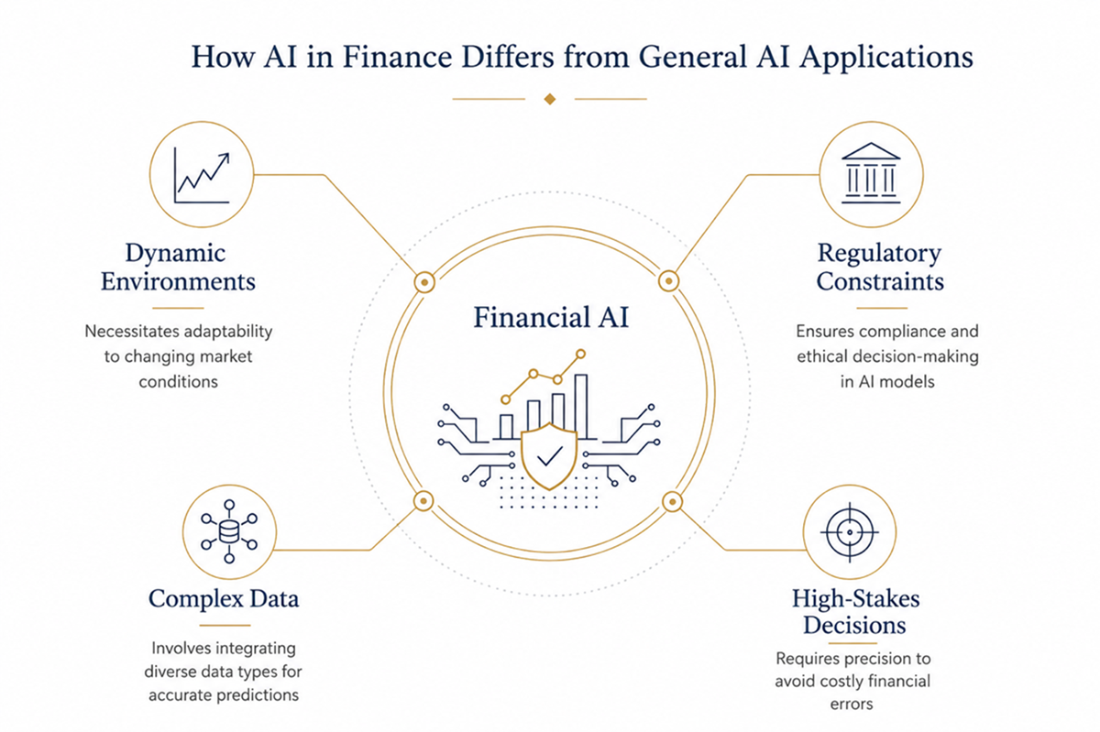

How AI in finance differs from general AI applications. Unlike many industries, finance requires continuous adaptation to changing markets, strict regulatory compliance ensuring fairness and explainability, uncompromising precision to handle high-stakes decisions, and the integration of diverse, complex data. These conditions shape every aspect of building and deploying effective AI-driven financial solutions.

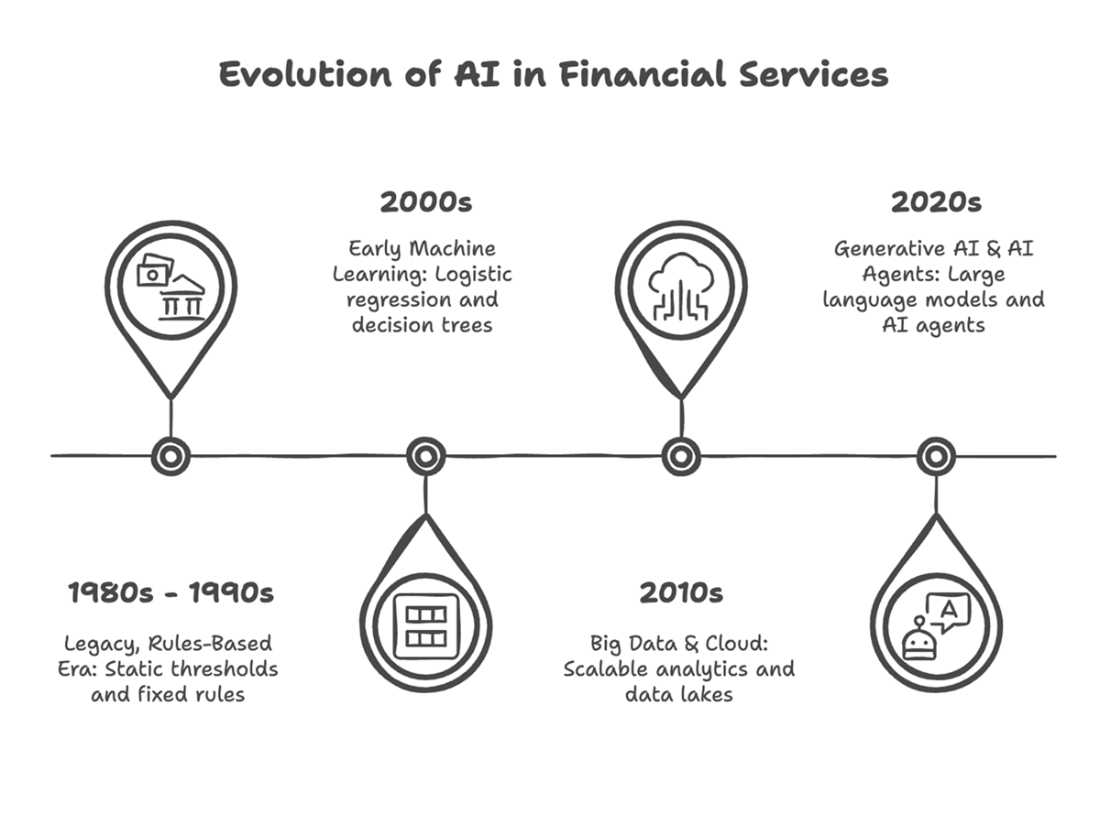

Evolution of AI in Financial Services. This timeline illustrates four major milestones in the industry's journey, from the static, rules-based systems of the 1980s and 1990s to today's generative AI and autonomous agents. Each phase—early machine learning, the rise of big data and the cloud, and the current wave of large language models—expanded AI's capabilities and its impact on the competitive landscape.

A four-layer mental model for financial AI applications. Financial AI applications are not just trained models or user interfaces. They connect curated data assets, predictive or generative models, strategy and monitoring rules, and application workflows. Feedback from real-world outcomes flows back into the system, helping teams refine data, models, thresholds, and operational decisions over time.

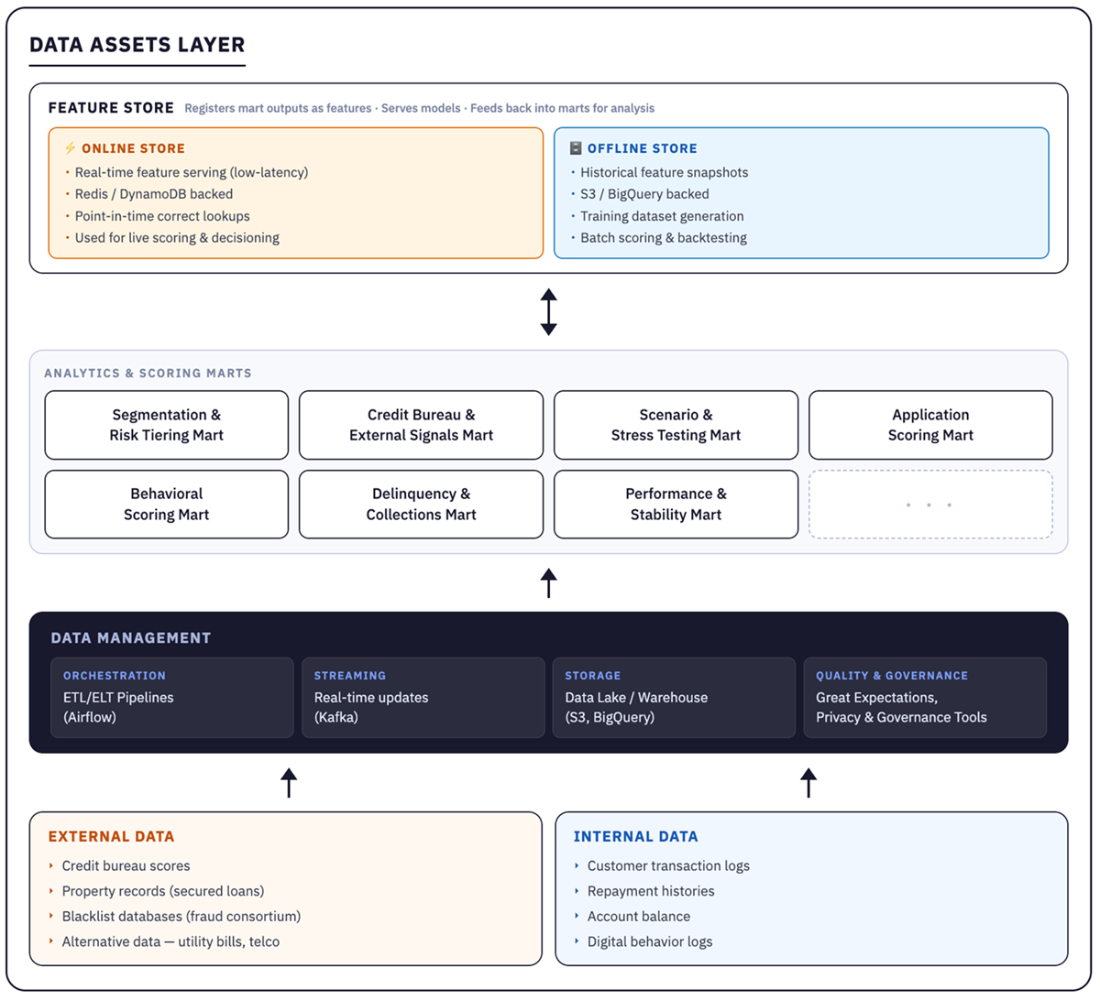

The Data Asset Layer. This figure illustrates how raw data—repayment histories, credit bureau snapshots, and alternative signals—flows into specialized data marts. Ensuring data lineage, access control, and regulatory compliance are critical steps before modeling. By creating consistent, domain-focused features, the Data Asset Layer provides a solid foundation for accurate credit decisions.

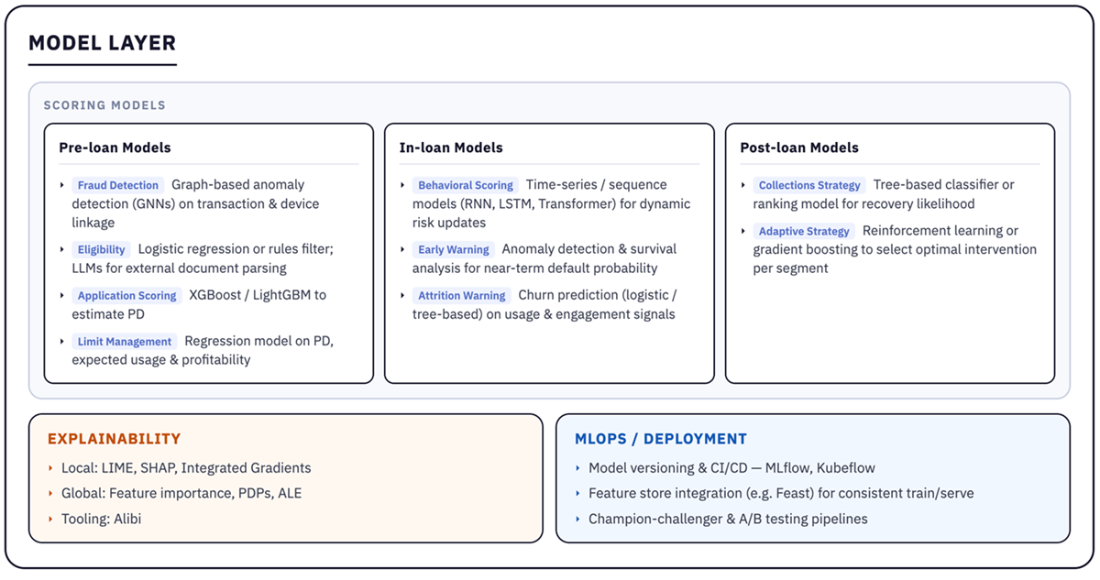

The Modeling Layer. Here, AI models turn curated features into default probabilities, fraud signals, or risk segments. Explainability tools (e.g., LIME or SHAP) offer transparency into each factor’s influence on the final score. Ongoing MLOps practices—such as scheduled retraining or hyperparameter optimization—help keep models current in shifting economic climates.

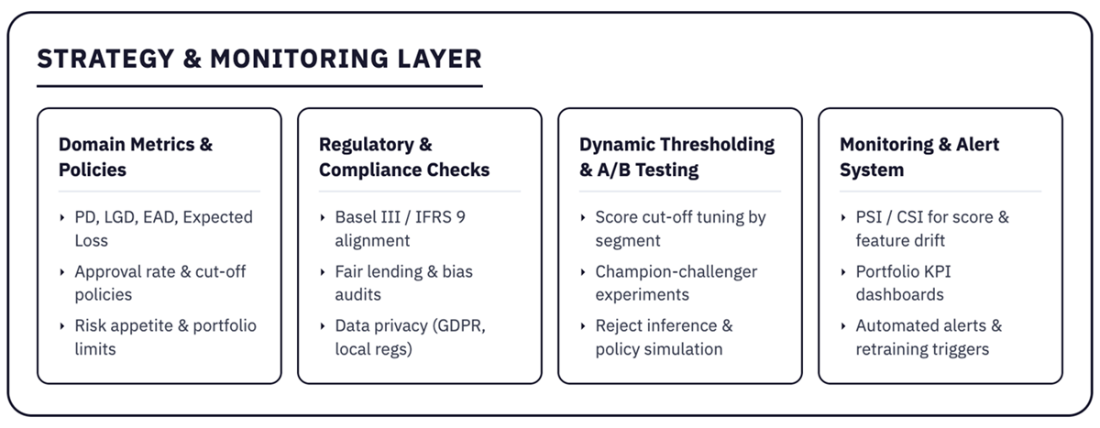

The Strategy & Monitoring Layer. Domain metrics, rate caps, and threshold policies shape how raw scores become lending actions. Ongoing monitoring detects data or concept drift, ensuring the model’s real-world performance remains stable. A/B testing and other experimentation approaches allow teams to refine credit strategies without risking large-scale exposure.

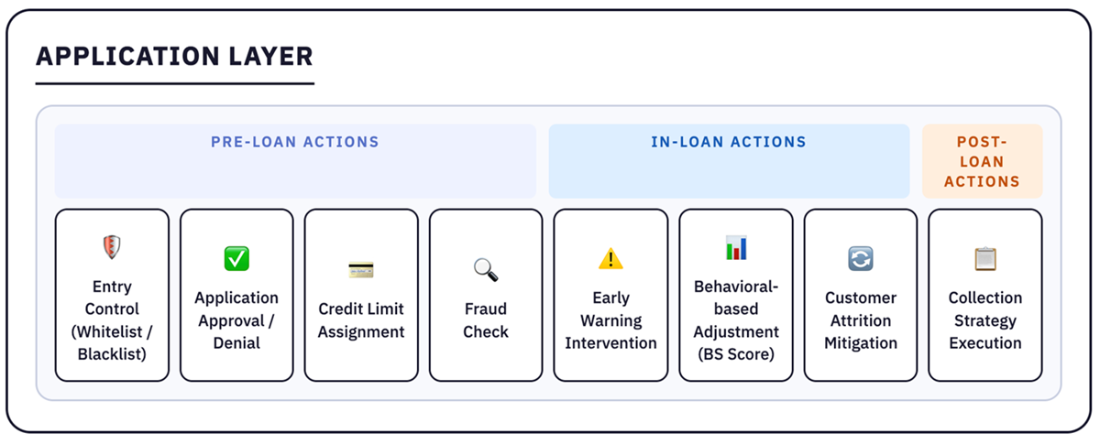

The Application Layer. Loan officers, collection agents, and end customers interact with AI-driven outcomes via dashboards or real-time notifications. By bridging front-end systems (like customer portals) and back-end rule engines, actions like approvals, limit changes, or fraud checks happen seamlessly. Because it’s closely tied to monitoring feedback loops, the Application Layer can adapt quickly to new data or policy shifts.

Summary

- AI in finance integrates data-driven modeling techniques into traditional workflows, enabling improved risk assessment, enhanced customer experiences, advanced trading strategies, and more streamlined operations.

- Understanding core building blocks—Data Asset, Modeling, Strategy & Monitoring, and Application Layers—helps break down complex AI systems into manageable parts.

- A concrete example in credit scoring shows how these layers interact: raw data transforms into predictive insights, which then guide policies and final lending decisions.

- Tools and technologies like Python, ML/DL frameworks, and optional orchestration and monitoring tools provide a flexible, accessible stack for building and maintaining financial AI solutions.

- This book teaches AI in finance through hands-on projects, real-world datasets, domain-specific metrics, and evolving model lifecycles—equipping you to adapt these methods beyond the examples given.

- Financial AI applications should be treated as evolving systems rather than one-time modeling exercises; they require continuous refinement as data, markets, regulations, and user behavior change.

Financial AI in Practice ebook for free

Financial AI in Practice ebook for free